ProSight Banking Outlook

2025 Small Business Trends

Get Started

In 2025, businesses of all sizes are balancing growth ambitions with rising operational pressures and the persistent challenge of fraud.

Meanwhile, shifts in preferences in banking and the integration of proactive relationship management are reshaping how small businesses interact with financial institutions. Supported by detailed data and actionable insights from the annual ProSight Small Business Outlook survey, this gbook examines the emerging trends and pressing challenges impacting small businesses and the financial institutions that serve them.

Read On

Growth as the Top Priority

61%

46%

34%

49%

32%

44%

35%

51%

33%

<$1M

$1M-<$5M

$5M-<$10M

$10M-$20M

annual revenue size

top priorities

Growth is critical, with just over 50% of business ranking it as their top challenge.

Growth Cash flow Cybersecurity Operational efficiency Technology investments

key

The Rising Threat of Fraud

With nearly 60% of businesses citing fraud as a significant concern, financial security continues to be a focal point for businesses and their banking partners. Institutions offering visible fraud mitigation solutions are better positioned to retain their clients. Businesses are adopting multiple strategies to combat fraud.

Require dual authorizations for significant financial transactions.

Review account and financial statements to catch discrepancies.

Invest in fraud detection tools to flag unusual transaction activity.

Leverage cybersecurity tools like firewalls and antivirus software.

Fraud prevention is not purely a financial defense mechanism; it strengthens relationships built on transparency and reliability. Businesses that feel secure are more likely to deepen loyalty to their financial partners.

Changing Banking Preferences

Local banks and credit unions have seen a decline of 3% year-over-year as the primary financial provider for small businesses. Meanwhile, direct/alternative banks are experiencing 5% growth annually. While large banks continue to serve the majority of small businesses, their market share has declined by roughly 2% year-over-year.

A growing shift to alternative providers

Businesses under $1M in revenue are more likely to choose direct/alternative banks (24%), whereas only 6% of businesses generating $10M-$20M consider these options.

View The Data

24%

5%

4%

1%

20%

11%

68%

17%

9%

69%

21%

6%

79%

18%

Direct/Alternative Local bank or CU Regional bank Large bank

Main business financial provider by annual sales size

Lowest fees

Best products

Positive reputation

Services that help run their business

Best rates

Why do businesses switch?

Dual-provider strategy

There is increased demand for specialized services:

52% of businesses use more than one provider for deposit accounts.

This dual-banking approach highlights opportunities for traditional financial providers to innovate and expand service offerings, particularly in areas like competitive merchant services and advanced digital platforms.

40% rely on multiple providers for loans.

A major change from 2024 is that “best rates” is no longer one of the top five reasons to shift service providers, underscoring the loyalty that is tied to trust, advisory services and adequate support structures.

Digital and branch preferences

of small business owners prefer utilizing branches for account creation, while mobile trails behind at 29%.

of interactions now involve digital and self-serve channels.

Mobile and online preferences continue to outpace other channels, reinforcing the importance of user-friendly and secure digital banking tools.

Small business owners aspire to leverage digital channels for account openings but often face roadblocks that prevent this, like identity verification.

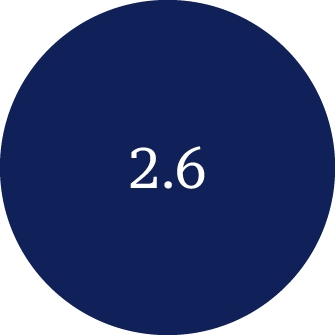

The Role of Relationship Managers

Businesses with revenue between $5M-$20M maintain these partnerships for an average of 2.6 years, reflecting the stability and trust inherent in such relationships.

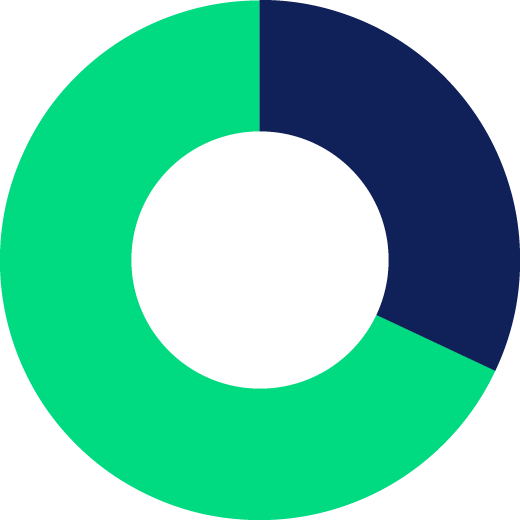

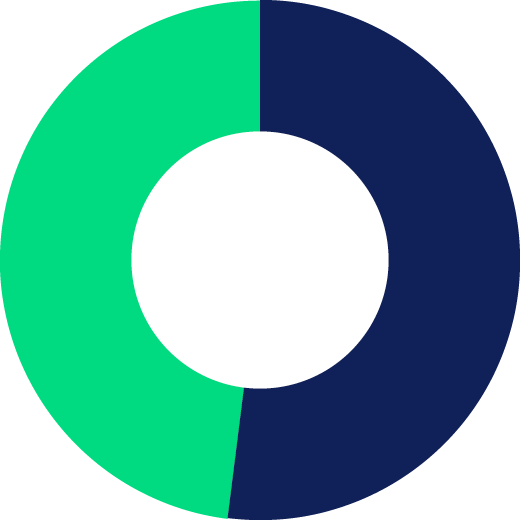

Do you have a relationship manager?

The role of relationship managers cannot be overstated. Larger businesses value these professionals as critical partners in their financial strategies:

Yes

No

By annual revenue of business

Average tenure of relationship manager

IN YEARS

Relationship managers are critical for goals like:

Helping businesses manage operations effectively Educating clients on digital solutions to streamline processes

Advantages of relationship managers

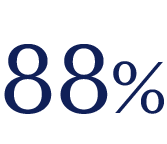

of businesses earning $1M-$5M say their provider calls them at least quarterly, creating ongoing opportunities for personalized advice.

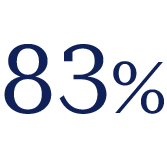

of businesses earning $10M-$20M agree their financial provider is well-integrated into their business operations.

Offering similar advisory services to smaller businesses could unlock growth opportunities and increase client loyalty for financial providers.

Looking Ahead

The financial industry moving into 2025 will be defined by heightened competition, evolving customer expectations and ongoing risks. Key considerations include:

Enhancing fraud prevention tools and educating businesses on evolving risks

Expanding digital channels to deliver seamless, intuitive banking experiences

Strengthening relationship management programs, especially for smaller business segments

By addressing these priorities, financial providers can build deeper trust and better support the diverse needs of their clients, ensuring mutual success in the years ahead. Learn more about how ProSight research can help financial institutions make smarter business decisions by viewing our latest webinar or get in contact with us today.

Watch The Webinar

Contact Us

Start Over